Over the last couple of years with the rise of ‘Democratic Socialism’, aka Socialists masquerading as Democrats, the idea of free college has been making a lot of headlines and gaining some traction within certain circles.

Although entirely flawed, the premises for this idea is as follows: There isn’t enough job opportunity without college degrees, which has resulted in unemployed and underemployed Americans, and the only remedy to this is to get more kids into college. Because without a college degree, people become criminals. But we can’t send more kids to college because it’s too expensive. Rather than finding ways to make college tuition itself less expensive, let’s simply pay an exorbitant amount of money to send everyone to college ‘for free’.

So that’s the idea. That horribly flawed chain of thought has led to the popularity of Bernie Sanders. In fact, Bernie said:

Providing a path for kids to go to the University of Iowa is a hell of a lot cheaper than providing them a path to go to jail. #iacaucus

— Bernie Sanders (@BernieSanders) December 14, 2015

Implying that if you don’t go to college, you’ll go to jail, which is the roundabout way of accusing anyone opposed to jacking up taxes to pay for every kid to go to college as a heartless person who wants to see more minorities end up prison. Essentially.

But the fact is that college isn’t all that. There are plenty of ways to become successful without a college degree.

What has me annoyed and disgusted the most with this whole notion of free college for everyone is that it’s based on a series of false notions, it presents a false dichotomy, it attacks symptoms rather than root causes, it’s redundant, and it would in fact have the opposite effect as intended – meaning it would cause tuition to increase thus making college even less affordable, all of which I will explain below and back up with logic.

Camp Kool-Aid

These days most colleges are simply liberal indoctrination camps. I think a huge part of the reason for Democrat’s wanting more of America’s youth to go to college is to drink the liberal kool-aid and eventually join the ranks of the Democratic party. With their anti-free speech safe spaces, pro-Hamas antisemitism rallies, and trying to oust ROTC and Border Patrol kiosks from campuses and job fairs, you can see how today’s American college campus is the perfect breeding grounds for American liberalism.

Many college campuses are now not only anti second amendment, they are also anti first amendment with students and faculty being suspended, expelled, or fired for expressing things considered to be offensive.

False Dichotomy

Forget for a moment the political posturing related to the free college discussion, and lets circle back to what caused it in the first place. If you ask Bernie Sanders, we need to send kids to college because if we don’t they’ll likely end up in prison. That’s the false dichotomy being presented by the liberal left to America’s youth today: Get a college degree or fail at life.

In response to a like remark made by Sanders, television personality Mike Row had some very interesting things to say where he gives myriad ways to become successful without college, include his personal experience.

Neither my mom nor dad have college degrees, but both are very successful. But what about my generation? Some friends my age, who I went to high school with and who don’t have college degrees are also very successful. I know a handful of people who have college degrees and aren’t successful. And there are people like myself (I consider myself successful) who have a degree and don’t use it in the slightest bit. Had I known I could make as much money as I do without a college degree, I would have never gone to college and started out in my career five years earlier. Just don’t tell my mom.

The always-and-only-college mentality has left a huge blind spot in the American workforce. We’re actually experiencing a shortage of much needed occupations such as plumbers, electricians, mechanics, and other blue collar and vocational related trades. Despite the fact that one can make a good living without working at a desk from 9-5, certain occupations have been framed by society as being lowly, which is a shame.

College Isn’t for Everyone

It’s a waste of money to effectively give every student free education because many of those students will end up pissing away the money we spend on sending them to school. Not every person is made for college. This isn’t to say they are stupid, but that college is a very specific model that isn’t compatible with how everyone learns and thrives.

I have a close friend that has been in college for well over eight years without any measurable progress. A relative of mine has been in college for 11 years without any degrees to show for it. No bachelor’s degree. No associate’s degree. I love both of them, but they are real life Van Wilder’s, and I think it’s safe to say neither of them will get a college degree.

I certainly don’t think it would have been a good idea to subsidize their education with anyone’s tax dollars because it is clearly working out to be a poor investment. My friend and relative are just two people out of nation of millions. Imagine how many other students would find themselves in similar predicaments, and how much tax payer money would be wasted on a large scale if we sent everyone to college.

Musical Chairs

Taking the previous point and expanding on it, aside from the cost factor of sending incompatible students to college, doing so would also make it increasingly difficult for students who legitimately could benefit from college. As it stands, most US colleges are already impacted. Kids with 4.0 GPAs and all the right motivation have a hard enough time as it is getting into the college of their choice, and the class and programs needed to complete their curriculum. And that’s with tuition costs being as astronomical as they are. If we lowered the bar so much that anyone with a pulse could join college on a whim, imagine how much the current problem would be exacerbated.

Cause and Effect

I don’t think too many ‘Berners’ have really put any thought into why college tuition costs are as high as they are – the root causes. Instead, all their efforts are focused on the ‘evil banks’ that finance student loans, – the symptoms – but for some reason they don’t have the same animosity towards the genuinely evil college system that charges such exorbitant rates in the first place.

After all, if colleges weren’t ripping students off with such high tuition, the student debt problem wouldn’t be so much of an issue. And if colleges are being such douche bags and ripping off students, why are parents so hell bent on sending their kids there? How can a liberal dominated college system be both the cause and solution to all of your financial woes?

Pro-college people argue that you need to go to college to get a good job to make money. And these same people are the ones reeling from hundreds of thousands of dollars of student loan debt accumulated during their stint at liberal colleges. So what is college? Plague or panacea?

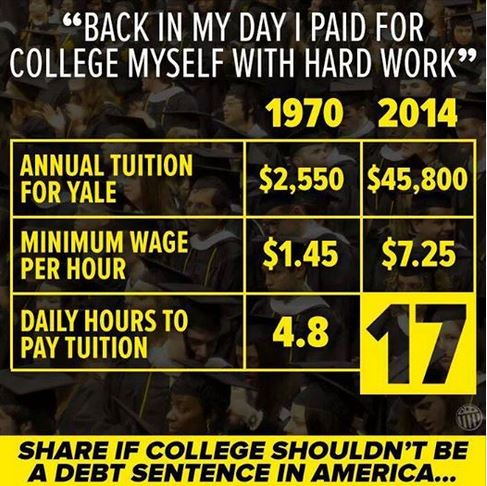

Another relative of mine posted the following image on Facebook back in February that shows the tuition change at Yale from 1970 to 2014, against the federal minimum wage of the time. Oddly, the image’s point is to use higher tuition costs as justification for increasing the minimum wage, as opposed to attempting to simply lower tuition costs, which are arbitrarily set.

I did some homework. Let’s say this image is accurate and that the tuition at Yale went from $2,550 in 1970 to $45,800 in 2014. That is 17.96 times higher, or a 1696% increase.

We’ll yeah Andrew, it’s called inflation! Duh! Just one minute though…

If we take that 1696% and divide it by the time span in years to get an average tuition percentage change per year, we get 1696 / 44 years = a 38.54% annual increase in tuition.

Compare that with the average US inflation rate of 3.22% over the last century, or even the average US inflation rate over that same period of time (1970 through 2014) of 4.08% (sources). Using these historical figures, Yale’s tuition grows nine times faster than inflation.

Basically, if Yale’s tuition moved at the rate of inflation, that $2,550 tuition in 1970 would have been about $14,815 in 2014. So why was it $45,800 instead? Maybe the problem here isn’t the banks financing the tuition. Maybe the problem is the universities who set the tuition. And perhaps supporters of more affordable college need to be scrutinizing the universities they hold in such high esteem.

Gateway to Extortion

The irony of this whole thing is that there is no surer way to increase college tuitions costs than by giving everyone free college. Liberals are determined to get free college for all at any cost, and they might succeed in ways they didn’t hope to.

If colleges around the country know that the US Government is writing blank checks to cover college tuition, what do you think is going to happen to tuition? It’s going to skyrocket. And it doesn’t matter what kind of clever legislation our politicians throw into the mix, the colleges are cleverer, and somehow, someway, they’ll find a way to take advantage of the situation and rip off the taxpayers.

Frugal Alternatives

These days, those of the left persuasion believe that the solution to any problem is to throw more money at it. This has led to the false belief that if you spend a ton of money on college as opposed to less money on technical or vocational school, it will always translate into higher pay. Or that a degree from an expensive, prestigious university will provide for better job opportunities post college.

Both of these myths have been largely debunked, and even in the rare instances where say a degree from Harvard will earn you higher income than a degree from SDSU, the extra income is negligible, and actually comes at a loss when taking into account the net difference between post-graduate pay and overall college expenses. If you spend 2x more on tuition, and make even 5% more per year after college, it would take you 20 years of working to justify (earn back) the higher tuition cost.

Many students want to go to the college of their dreams. And while following your dreams sounds, well, dreamy, when dreams start to conflict with reality there’s a problem. These students insist on attending some far away university, where they’ll get strapped with significantly higher out of state tuition costs, plus the added expense of room and board. All of which they could have avoided by simply going to a local, in state university and living with their parents for at least a portion of their college career.

Ultimately, college is a financial decision. Not an emotional one. So students, and more importantly their parents, need to start looking at college options closer to home where they can take advantage of the lower in state tuition. Take it a step further and consider attending a community college for as many semesters as possible and students can save tens of thousands of dollars per year on their education.

My freshman, sophomore and junior years were spent at Grossmont Community College where my cost per semester was about $600 (with books) as opposed to the $5,000-$7,000 it would have cost me at SDSU. I transferred to SDSU in my senior year where I finished my bachelors degree and graduated in the spring of 2009 alongside all my friends who went there for all five years, but in the processed I managed to save about $30,000.

We all want to have our dream house, our dream car, our dream vacation, our dream wedding, and go to our dream college, but the simple truth is that those things are often times cost prohibitive and well beyond our budget. It’s stupid to spend $50,000 on a BMW when you can only afford a $25,000 car, and it is just as stupid to attend an expensive college when you can get a degree every bit as good for a quarter of the cost. Some community colleges are also beginning to offer bachelor’s degrees of their own, negating the need for costly universities altogether.

Borrow Wisely

Another problem is that many students simply borrow when they don’t have to. Student loans should be used to cover tuition and books, and not much else. However a lot of students will finance everything they purchase while in college, from housing, to food, to luxury items like recreational spending and even overseas vacations.

This is unwise for a number of reasons. The whole point of a student loan is to pay off an expense you otherwise would not have had: college. However whether you attend college or not, everyone has food costs, housing costs, clothing costs. Just because you are in college, doesn’t mean your breakfast while in college is a college expense. It’s a living expense. Everyone has to eat. Students make the mistake of financing things they would have had to pay for even if they hadn’t gone to college. The result is that when they graduate you aren’t simply paying off five years of deferred tuition, they’re paying off five years of deferred life.

Additionally, students should actually start paying off, or saving to pay off, their debt while they are still in college. When you consider that student loans are basically the only loans in which the borrower is not charged interest for up to half a decade, student loans are actually the most relaxed form of lending on the market. You have 0% financing for 60 months! Don’t wait until graduation to start paying off your debt. Start on Day 1 of freshman year.

Reinventing the Wheel

The other hilarious thing about this recent sensation is that programs already exist to get college loans paid off easier, quicker, and so inexpensive that it is essentially debt forgiveness. About ten months ago I posted a blog written by my cousin-in-law Chris Johnson titled “The Truth About Federal Student Loans” in which he describes in amazing detail the government programs that have existed for decades to help alleviate student debt, and how such programs are alive and well today. It’s funny because democrats are crying for something that already exists.

In Conclusion

Liberals want to send more kids to college to be brainwashed into becoming liberals themselves.

There are many pathways to success, many of which do not included college. College is not a requisite for success.

Not every kid would do well in college, therefore giving every student free tuition would be a gross waste of money.

Because schools and courses are already impacted, sending ill-suited kids to college would jeopardize the education of students who actually are suited for college, by making it even harder for them to enroll in the classes needed for their degree and by spreading professors thin.

Yes, college tuition is high, but don’t blame the banks for student debt. Blame the universities for ripping-off the American public. Colleges across the country have routinely increased their tuition at a rate much higher than inflation would account for. Colleges need to be brought to task, not the lending institutions.

High tuition costs are avoidable though. By attending state universities and taking your general education requirements at a community college students can cut the cost of college in half.

Only finance college costs. Do not finance general living expenses. Students and parents should start paying off, or saving to pay off student loans from the very beginning. That debt should not be ignored simply because it is not yet due.

This is the truth behind, and the solution to the United States current student loan crisis. The fact is, college isn’t all that.